$LSF is just getting started

Laird Superfood isn't getting enough credit for their turnaround

Company: Laird Superfood

Ticker: $LSF

Price: $2.60

Market Cap: $24.7M

EV: 18M

Summary:

A new, overqualified CEO has restructured a severely unprofitable DTC brand into a breakeven, rapidly growing CPG company. One year ago, Laird looked like your typical failed DTC brand: marketing at 40% of sales, gross margins in the low 20s, and a plethora of operational issues. With CEO Jason Vieth at the helm, the company doubled gross margins through 3rd party manufacturing and streamlined SKUs, cut marketing in half by prioritizing high ROI ads, and grew wholesale channels significantly. Today, shares trade at just .45x EV/Sales for a well-capitalized, high margin lifestyle brand growing at double digits annually. If current brand momentum continues, LSF is poised to inflect to profitability in 2025 then compound net income at >50% annually with potential to nearly 10x its market cap over 5 years.

Company:

Laird Superfood is a celebrity brand founded by volleyball player Gabby Reece and surfing icon Laird Hamilton. The brand focuses on creating energizing supplements, coffee creamers, snacks, and drinks made from real-food ingredients. In 2021, the company IPOed at a $184M valuation and took off after huge increases in sales, but then growth dissipated. The stock price plummeted 90% to its net cash position, which shrank quarter after quarter due to low margins and high marketing expenses.

Current CEO Jason Vieth took his role in the midst of this disaster, and immediately sought to improve margins and lower operating expenses. He switched manufacturing to 3rd parties, cut ineffective marketing, reduced SKU count, relied more on Laird/Gabby to promote the brand, and reduced corporate headcount to 25 employees. Though he came at a time when the company was in free fall, his changes have yielded results and repositioned the company for growth.

Entering 2024, Laird is projecting gross margins from 37-41%, and sales growth of 10-22%. Furthermore, while they did not state this outright, snippets from earnings calls suggest that OpEx will be $8-9M and marketing as <20% of sales. They will likely be net income positive for the 2nd half of the year, but only be profitable for the full year if they raise guidance. Regardless, with 90% of their revenues coming from repeat customers and 50% coming from subscriptions, they should exit 2024 with considerable momentum.

Let’s look at some drivers for growth:

Wholesale: On a recent call, the CEO said conventional wholesale expansion is at least one year out since they want to protect margins. Coffee creamers are >50% of the company’s revenues and a strong majority of creamer sales come from in person sales. Considering that they are a number 1 brand in Sprouts and have national distribution in Whole Foods, successful nationwide launch in general retailers would make revenues for 2025-2026 multiples of where revenue stands today. Furthermore, there is room for further penetration with existing partners (Whole Foods, Sprouts, etc). Retailer scanner volumes being up 30% last quarter as well as LinkedIn updates showing SKU expansion further demonstrating the health of the wholesale channel.

Strategic Marketing: Founders Gabby Reece and Laird Hamilton are true ambassadors of the brands with huge followings. The highest performing social media posts from LSF feature them. Shifting towards more collabs with them will not only improve lead to more revenue, but also reach an audience of high-performance athletes they may not hit otherwise. Management stated their ROI for marketing with them was always the highest and always generated the highest impressions.

Product Innovation: Laird has consistently demonstrated its ability to design and produce trendy superfoods ahead of the market. For example, years ago they started selling ‘performance mushrooms’ (blended mushrooms to mix into drinks), which now generate millions in sales. Furthermore, they capitalized on the recent AG1 hype (blended greens for people who don’t eat veggies), and generated millions off a formerly small product line in 2023. As more people shift to foods supercharged with nutrients they lack in their terrible diets, LSF has shown that they’re ready to capitalize on this with new products.

Industry Growth and Social Media: Clean, plant-based superfoods/supplements are becoming more and more popular. The organic industry growth will continue to be a huge tailwind for companies like Laird that focus on being extremely healthy/clean products. More specifically, Laird admonishes the use of “natural flavors”, which further differentiates them from many of the “clean” brands on the market. Social media and health influencers are putting the spotlight on clean ingredients and nutritional content, and this presents yet another tailwind for Laird beyond the general industry growth.

Current analyst projections of ~8% revenue growth for 2024-2025 seem unreasonably low, given the expectation of double-digit organic growth this year despite reduced marketing spending.

Market and Competition:

Coffee creamers and supplements are very competitive with little differentiation. Laird Superfoods leverages its celebrity brand to lower its CAC and improve brand awareness. Furthermore, their commitment to not using natural flavors and instead using only the highest quality ingredients makes it one of few nondairy creamer / supplement brands to do so. Their pricing is comparable to competitors for the majority of their products. Therefore, LSF is relatively differentiated, though like many CPG companies, there is no true moat here.

Catalysts:

One major catalyst is the company entering conventional grocery stores since this is the largest revenue opportunity. Once they decide to do so (and if they can), revenues would skyrocket through that channel and enhanced brand awareness would improve DTC sales as well.

Additionally, the stock nearly tripled upon releasing Q4 earnings that showed the potential to inflect to grow and improve margins. As the company continues to prove that it can execute and inflects to profitability, there is room for a significant rerating.

Price Target:

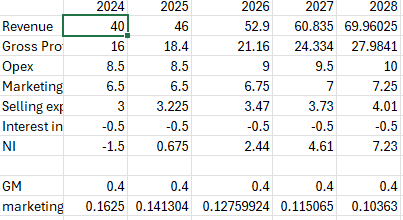

Before valuing Laird, let’s project some financials. 2024 is roughly based on the midpoint of guidance and the years onward reflect my estimates. The spreadsheet below should make one thing clear: this business model has incredible operating leverage if they can continue to grow revenues.

*140M in NOLs negates taxes

Management has indicated that in the midterm they want to get marketing as a % of sales to low teens, and in the long term, high single digits. I think a little faith is warranted given management’s track record. Furthermore, they expect OpEx to remain at current levels, selling expense to increase slightly, and margins targeted at ~40%.

The big assumption is revenue, but a 15% growth rate is achievable. Last quarter reported 10% wholesale growth despite their products being scanned 30% more. Thus, distributors destocking understated growth pointing to easy comps for 2025. The DTC channel also reported >20% growth in the last quarter. If management meets the midpoint of their guidance, revenue growth would be 16% for 2024, so with current brand momentum and wholesale expansion, they could even exceed this 15% threshold. It’s also worth noting that growth this year is without any price increases.

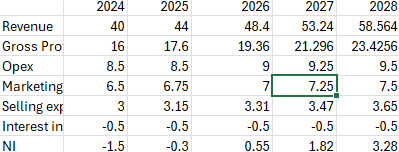

Even if we take a 10% growth rate, the outcome is still very attractive.

With a 15% growth rate, applying a 30x P/E to 2028 numbers shows a path to a ~$220M EV and a 10% growth rate yields ~100M.

Clearly, valuing LSF is challenging given the variance in outcomes, but a comparable company $LWAY trades around 1.6x EV/Sales despite being a far inferior business with questionable management. While Laird is smaller and breakeven, I think an EV/Sales of 1.5x is reasonable which yields an EV of ~60M. Based on 10M shares, this would yield a share price of $6.63 and upside of 155%.

Furthermore, in a blue-skies scenario where they successfully enter conventional wholesale channels and revenues exceed >$100M, a buyout could occur in a higher range of 3-5x sales. Danone is a large shareholder and acquired WhiteWave Foods at roughly 3x sales several years ago. At the time CEO Jason Vieth worked there as a brand leader in nondairy products, so this does point to Danone being a suitor.

Regardless, assuming they can maintain double digit growth rates for the next few years, shareholders will likely leave with far more money than they entered $LSF with.

Management:

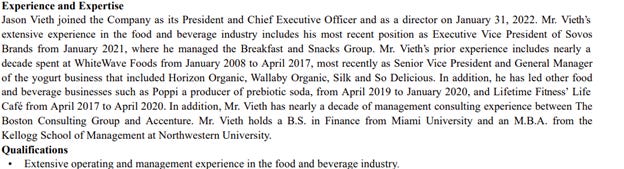

Management and the board are punching way above Laird’s current market cap. The board is full of former CPG executives who now serve on the boards of far larger companies. In particular, CEO Jason Vieth has an extremely impressive CPG resume. Here’ a paragraph on him:

Beyond their resumes, they have also earned credibility by exceeding every goal they set for this year. Furthermore, insiders have bought ~75,000 shares on the open markets in the last 3 months, showing further alignment with shareholders. Most importantly, Laird Hamilton owns ~7% of the company which reduces the risk of him abandoning the company for another venture.

Risks:

Management: Recently the company re-domesticated to Nevada to avoid lawsuits and save $200k a year. Nevada is far less shareholder friendly than Delaware, and this could pose a threat if management chose to stiff shareholders. Also, director compensation is very high at 100k per director for a $20M company. Insider purchases and a strong track record reduce this risk, but it is still concerning.

Celebrity Exposure: Laird Hamilton and Gabby Reece are important marketing partners to the company, and the loss of them or damage to their reputation would significantly hurt LSF’s brand. I don’t think either one poses a brand risk since they have settled down and now just reflect on their career instead of building on it. Additionally, their share ownership and compensation should prevent anything too crazy.

Conclusion:

As the adage goes, “Bet the jockey not the horse”. Management is overqualified for a $20M company and has done a phenomenal job repositioning Laird for growth. If you think they can maintain brand momentum over the next few years, this stock is easily a multibagger from here. While the market isn’t giving LSF much credit at just .45x sales, a multiple more typical for a distressed CPG company, this presents an attractive opportunity to buy organic growth and a potential buyout at a bargain.

Position Update:

I submitted this writeup to MCC about a week ago (got rejected), and since then there has been abnormal trading activity with shares almost doubling in price. I have not changed my position whatsoever and have no plans to do so since I think shares are still cheap at these levels (<1x sales). That being said, microcaps can react strongly to writeups only to correct shortly after, so I would encourage everyone to do their own research and consider the different risks before making a decision. Essentially, do your own DD and don’t ape into a small cap CPG company a college student researched. Feel free to DM me with any questions or feedback and don’t forget to subscribe and follow for more writeups.

Disclaimer:

I own shares. This is not financial advice. Do your own research.

Great write up! Credits to you for spotting this early